Welcome to GardenCities!

Welcome to GardenCities! Thank you for stopping by! We don’t take it for granted that you are taking time out of your busy day to check out our website. We are a small local real estate business in Springfield, VA. Our passion is to serve people whatever their real estate needs might be and create s

The Quiet Power of Green Space: How Where We Live Shapes How We Think

There’s something almost instinctive about the way we slow down when we step into a green space. A walk under mature trees, a quiet park bench, or even a small garden can shift the rhythm of our day. What feels calming in the moment may actually be doing something much deeper. A recent study publish

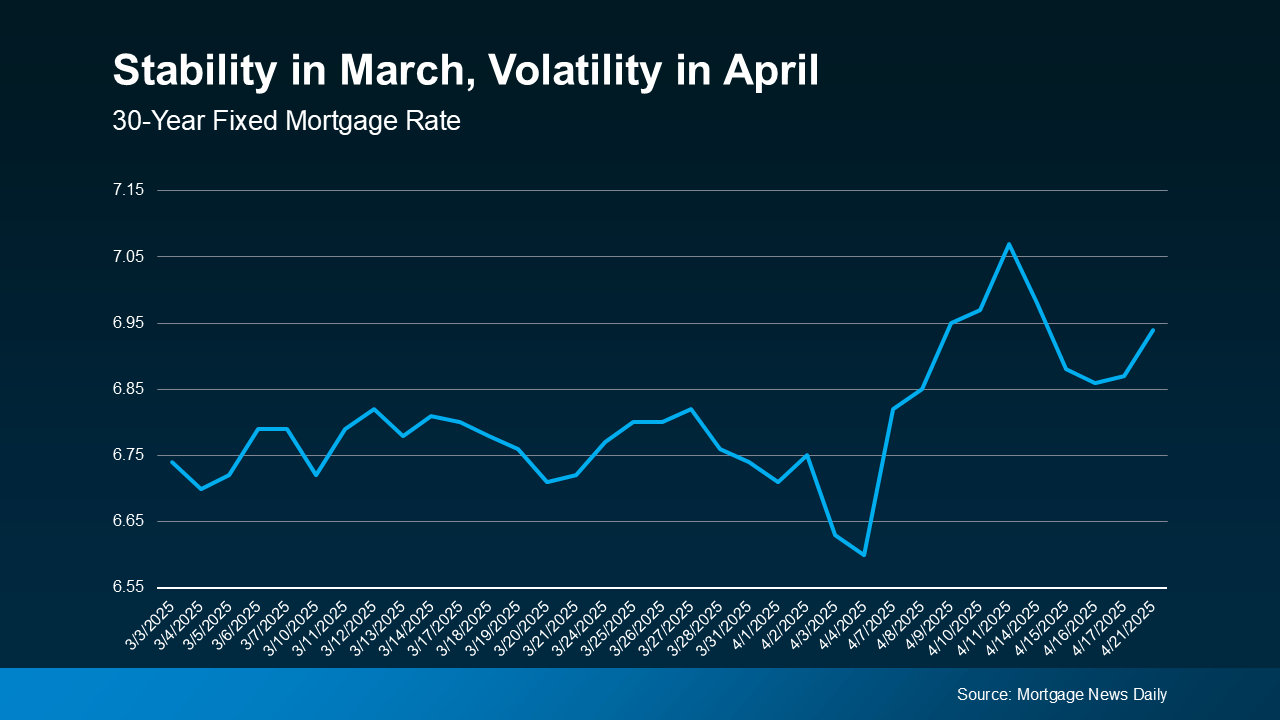

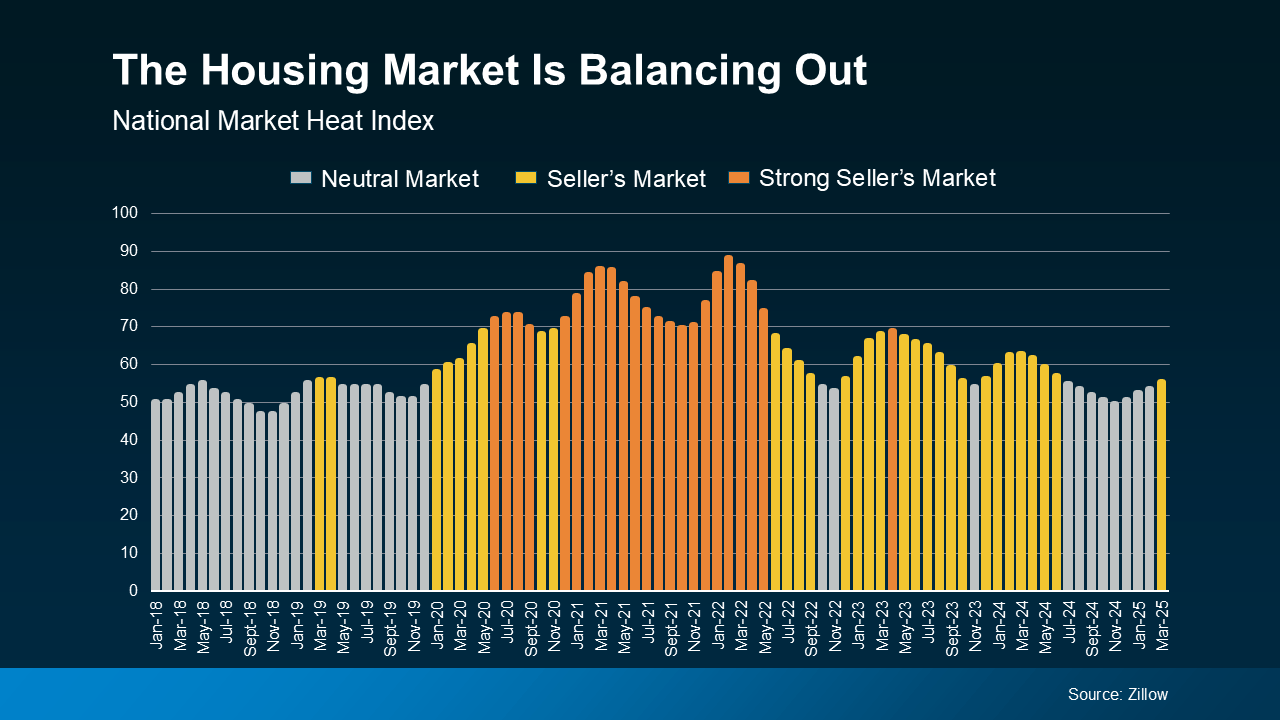

What an Economic Slowdown Could Mean for the Housing Market

Talk about the economy is all over the news, and the odds of a recession are rising this year. That’s leaving a lot of people wondering what it means for the value of their home – and their buying power. Let’s take a look at some historical data to show what’s happened in the housing market during e

Categories

Recent Posts