The Quiet Power of Green Space: How Where We Live Shapes How We Think

There’s something almost instinctive about the way we slow down when we step into a green space. A walk under mature trees, a quiet park bench, or even a small garden can shift the rhythm of our day. What feels calming in the moment may actually be doing something much deeper. A recent study publish

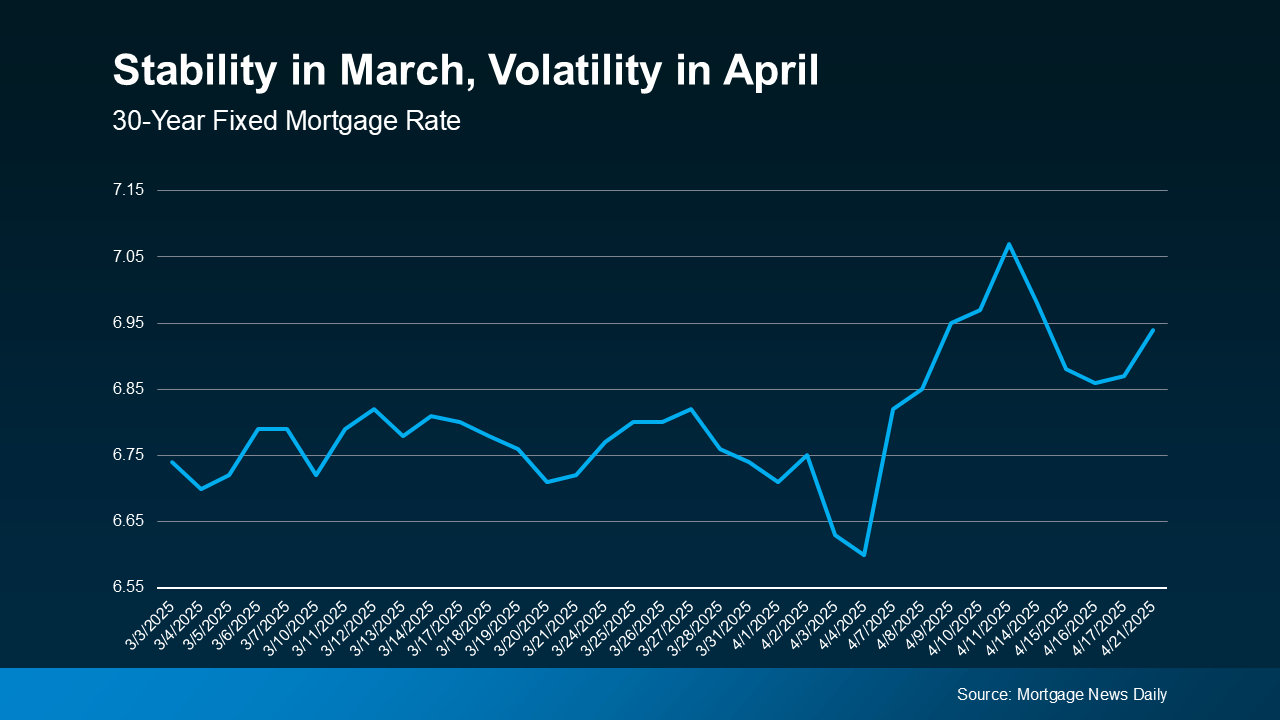

What You Can Do When Mortgage Rates Are a Moving Target

Have you seen where mortgage rates have been lately? One day they go down a little. The next day, they go back up again. It can feel confusing and even frustrating if you’re trying to decide whether now’s a good time to buy a home. Take a look at the graph below. It uses data from Mortgage News Dail

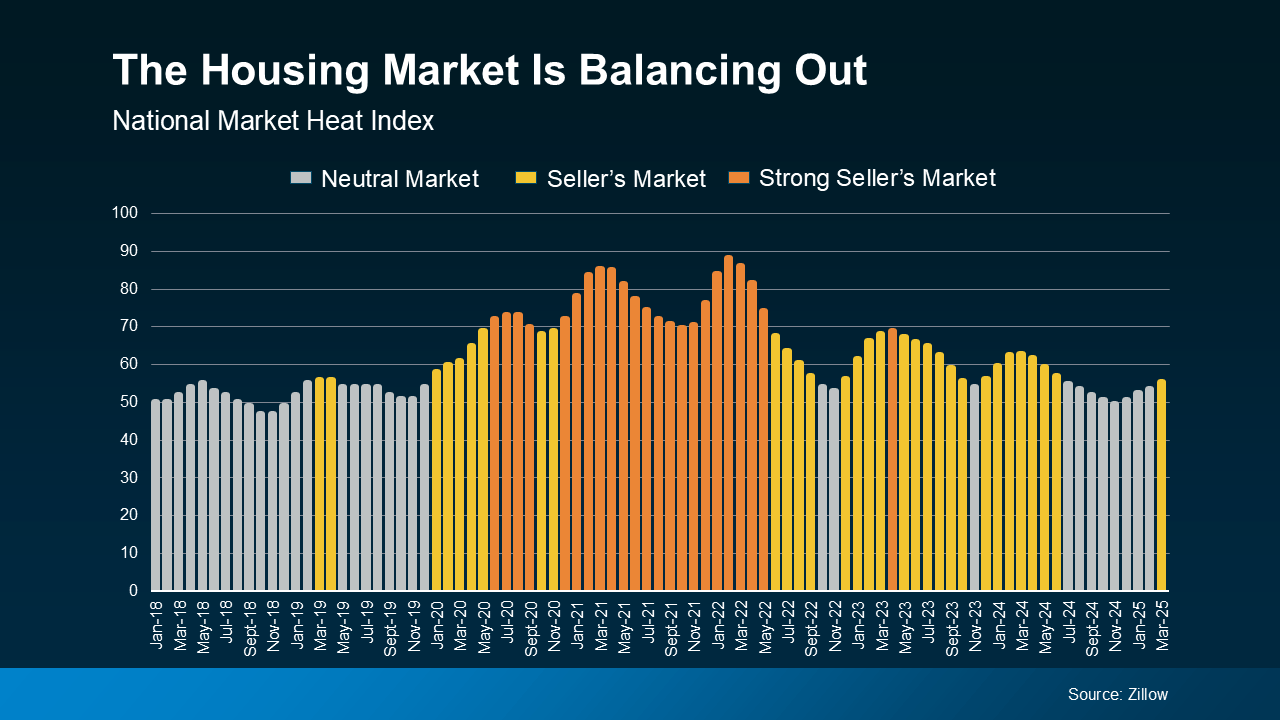

A Tale of Two Housing Markets

For a long time, the housing market was all sunshine for sellers. Homes were flying off the shelves, and buyers had to compete like crazy. But lately, things are starting to shift. Some areas are still super competitive for buyers, while others are seeing more homes sit on the market, giving buyers

Categories

Recent Posts